December 2025 CD Rates

| Bank Name | Account Name | APY | Minimum Deposit |

|---|---|---|---|

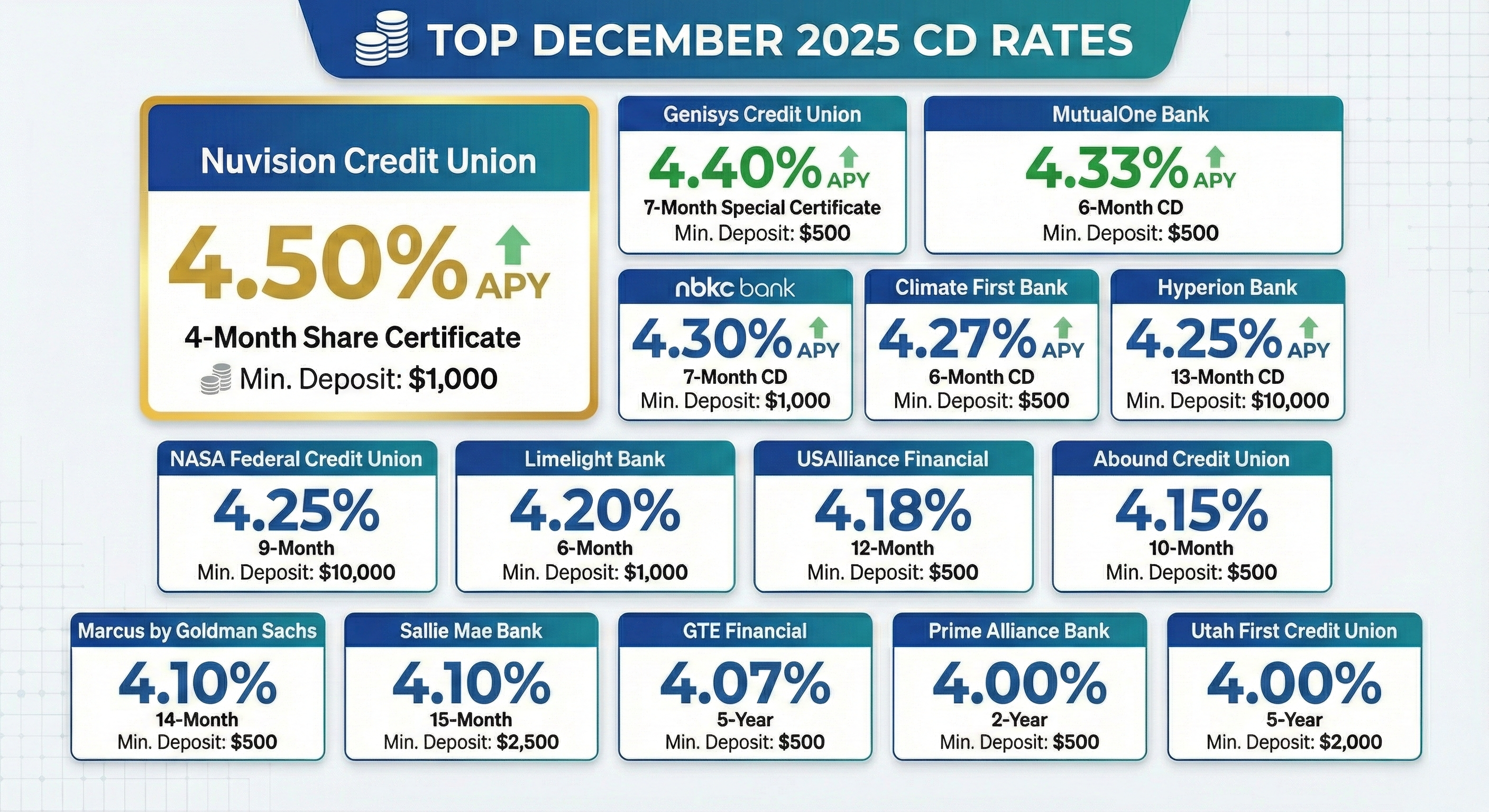

| Nuvision Credit Union | 4-Month Share Certificate | 4.50% | $1,000 |

| Genisys Credit Union | 7-Month Special Certificate | 4.40% | $500 |

| MutualOne Bank | 6-Month CD | 4.33% | $500 |

| nbkc bank | 7-Month CD | 4.30% | $1,000 |

| Climate First Bank | 6-Month CD | 4.27% | $500 |

| Hyperion Bank | 13-Month CD | 4.25% | $10,000 |

| NASA Federal Credit Union | 9-Month Share Certificate | 4.25% | $10,000 |

| Limelight Bank | 6-Month CD | 4.20% | $1,000 |

| USAlliance Financial | 12-Month Certificate | 4.18% | $500 |

| Abound Credit Union | 10-Month Certificate | 4.15% | $500 |

| Marcus by Goldman Sachs | 14-Month High-Yield CD | 4.10% | $500 |

| Sallie Mae Bank | 15-Month CD | 4.10% | $2,500 |

| GTE Financial | 5-Year Share Certificate | 4.07% | $500 |

| Prime Alliance Bank | 2-Year CD | 4.00% | $500 |

| Utah First Credit Union | 5-Year Certificate | 4.00% | $2,000 |

What Exactly is a Certificate of Deposit?

It’s never too early to begin building your nest egg. Safe and effective investments can help you slowly and steadily grow your savings. You may have heard the term “CD” commonly used in banking. If you’ve asked yourself, “What is a Certificate of Deposit?” you aren’t alone. Many people have heard the term but don’t fully understand what exactly it is. Basically, a CD is a savings account with some strings attached.

The Basics

A certificate of deposit, commonly referred to as a CD, is a time deposit account available at banks. Customers give the bank cash and agree to leave it in an account for a certain period of time. These safe investment options offer higher interest rates than savings accounts or money market accounts. However, the interest rates are generally lower than riskier investments, such as annuities or stocks.

CD Versus Savings Account

A CD is very similar to a savings account. Both earn interest and keep your money safe. CDs and savings accounts are both backed by the FDIC for up to $250,000. Unlike a savings account, you can’t freely withdraw money from a CD. The investment is locked in for a specified period of time, which is how long it takes the CD to mature.

Initial Investments

Most banks require a minimum investment amount to open a CD. The average minimum is $1,000, but some banks require $10,000 or more. The maximum amount banks will allow is often capped at $1,000,000 between one or several CDs. Since the FDIC only insures bank accounts for $250,000, it’s in the investor’s best interest to keep each CD below that amount. You can compare the minimum deposit for CDs with the Banks.org CD Comparison Table above.

Early Withdrawal Penalties

If you choose to take an early withdrawal, you’ll face a penalty. The exact amount you’ll lose varies based on the bank and the CD. You can expect to lose some interest and possibly even some of the principal you invested. Federal law only stipulates the minimum amount a bank can charge as an early withdrawal penalty. There is no maximum penalty amount regulated by law, but the bank must disclose this information when you open the account.

CD Terms

CDs are available in terms ranging from as little as a couple of months or as long as 10 years. Typically, a longer term is associated with a higher interest rate. The most common CD terms are about a year or two. Interest rates change daily. (You can view the most current rates by viewing the CD rate section of our site above.) If you choose a fixed CD, you’ll lock in the rate at the time of investment. If you opt for a variable rate CD, the rate will fluctuate based on the U.S. Treasury Note rates. At the end of your maturity date, you can withdraw the funds and interest or choose to roll the total into another CD. You can also take just the interest and invest the principal again.

No Penalty CDs

For those who don’t feel comfortable with the concept of not being able to touch their funds for several months or years, there are penalty-free CD options. These options are also called liquid CDs. Unfortunately, the freedom to freely withdraw your money comes with a lower interest rate than traditional CDs offer.

Taxes

All earnings on a CD are taxable in the year they are received. Your initial investment isn’t taxed, but the interest you receive is taxable income you’ll need to report to the IRS. Your bank will mail a 1099-INT detailing all taxable earnings at the end of the year.

If you’re looking for a stable investment option, CDs are an excellent choice. You’ll want to decide if the potential earnings from a CD’s interest rate is worth tying up your cash for several months or years. Everyone’s financial situation is unique. For some, a high-yield savings account is a good alternative to a CD because they provide more flexibility.